For years, video game music was treated as supporting material.

Important, yes. Memorable, often. But still secondary to gameplay, graphics, and the commercial value of the game itself.

That is changing.

Today, video game music is increasingly being treated as something that can live outside the game: as a soundtrack release, a streaming product, a live concert experience, a vinyl collectible, a sync asset, and in some cases a long-term rights catalog. Intel Market Research estimates the global video game music market at $1.295 billion in 2024, rising to $2.24 billion by 2032, while Cognitive Market Research forecasts a 12.4% CAGR from 2024 to 2031. The exact numbers vary, but the shared message is clear: game music is becoming a bigger business category, not just a production cost.

Game music is no longer just background sound

One of the most useful ways to understand the trend is to stop thinking about game music as only “audio inside a game.”

MIDiA’s argument is that video game music has gained much stronger cultural relevance as games themselves became mainstream entertainment. It points out that the Halo 4 soundtrack charted on the Billboard 200, which helps show that audiences do not always separate game music from the wider music economy. When enough players emotionally connect with a title, the soundtrack can begin to behave like a music product rather than just a gameplay component.

Intel reaches a similar conclusion from a market perspective. It explicitly says game music now generates revenue beyond the game through streaming platforms like Spotify, Apple Music and YouTube, and through live orchestral shows built around major franchises. In that framing, the soundtrack is not only a cost of development. It is a secondary monetization layer.

That shift is the foundation of the whole trend. You cannot really “sell game music” at scale until the market starts treating it as a standalone object of demand.

The market opportunity is growing, even if estimates differ

The sources you shared do not give one single agreed market size, but they do point in the same direction.

Intel Market Research estimates the global video game music market at $1.295B in 2024, growing to $1.39B in 2025 and $2.24B by 2032, which implies 8.3% CAGR. Cognitive Market Research projects 12.4% CAGR from 2024 to 2031. Those are not identical forecasts, and that matters. It suggests methodology differences, category-boundary differences, or both. But from a strategic content angle, the useful conclusion is that multiple analysts see a meaningful growth story here.

Intel also gives useful shape to the opportunity. It says in-game music holds the dominant share, mobile is the leading application segment, original composition is the dominant business model, and AAA titles dominate by production scale. That suggests the market is still rooted in core game production, but with the strongest upside likely going to soundtracks and franchises that can escape the game and find life elsewhere.

So the trend is not just “more game music exists.” It is that more of it is becoming commercially reusable.

What is driving the trend

There are a few reasons this is happening now.

First, gaming itself remains massive. Intel frames the video game music opportunity as downstream from the broader expansion of the games market and the rising production values of modern games. The more games compete on immersion, storytelling and brand identity, the more music becomes part of the product’s differentiation.

Second, soundtracks have become easier to distribute and monetize. Streaming platforms allow publishers and composers to release OSTs globally at low friction, while fan communities can keep those tracks alive long after launch. Intel explicitly identifies streaming and soundtrack-album monetization as a major driver.

Third, game music now performs better as an event format. Intel points to successful touring productions like Distant Worlds and Symphony of the Goddesses, which show that iconic game music can generate revenue in live settings too. That matters because it expands monetization from digital consumption into ticketed experiences.

Fourth, technology is pushing quality upward. Intel highlights spatial audio, adaptive music systems, and more sophisticated sound design as growth drivers. Better technology tends to make music more integral to the game experience, and that increases the odds that players will later value the soundtrack on its own.

The friction points are real

The opportunity is growing, but it is not easy money.

Intel lists several meaningful obstacles: high development costs, licensing and rights-management complexity, technical implementation challenges, market saturation, and piracy. In practice, that means not every studio can afford a sophisticated original score, and not every composer can easily turn a score into a durable revenue asset.

There is also a pricing problem. Intel says competition is intense enough to push prices down, especially for mid-tier and indie work. That means creators often face a familiar trade-off: accept lower upfront fees for access to the project, or negotiate for rights and long-term value in a context where bargaining power may be limited.

This is where game music begins to look a lot like the rest of the music industry. Demand grows, but creators still need strong rights strategy or they risk building value they do not fully capture.

A good example of game music strategy is MOUSE: P.I. For Hire: they start selling their music through digital channels such as BandCamp and put the full soundtrack in Youtube and Spotify.

Other examples of games that have tried to monetize their soundtracks include Gris and Hollow Knight / Silksong.

Alternative ways to earn royalties from your soundtrack

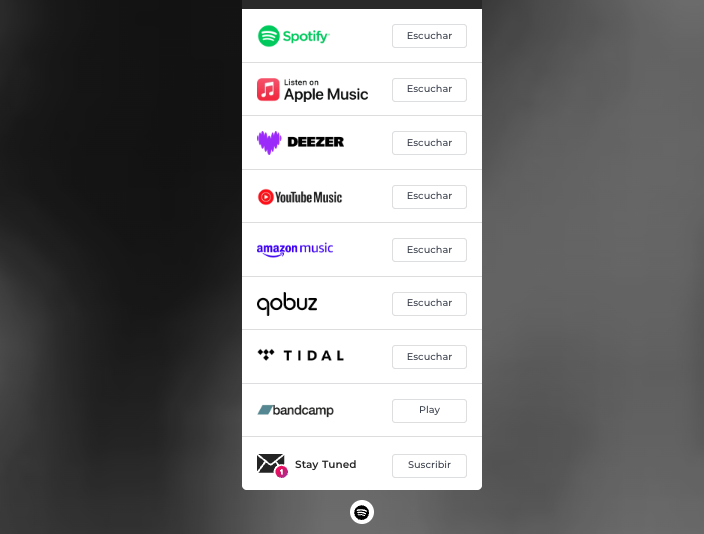

Another reason game music is becoming more valuable is that composers no longer depend on a single monetization path. One soundtrack can live across multiple platforms at the same time — Spotify, Apple Music, Deezer, YouTube Music, Amazon Music, Qobuz, Tidal, Bandcamp, and even email subscription channels.

That creates several royalty and revenue layers around the same work: streaming royalties from DSPs, direct sales through platforms like Bandcamp, fan retention through mailing-list signups, and stronger discoverability that can later lead to sync, live performance, or catalog opportunities. In practice, this means a game soundtrack does not have to stay trapped inside the game itself.

When it is properly distributed, packaged, and promoted as a standalone music product, it can generate recurring income across streaming, direct-to-fan sales, and long-term audience building — which is exactly why ownership, metadata, and rights management matter so much for composers and rights holders.

Why the wider music market matters too

One useful contextual source here is the Advanced Television piece on UK ERA data.

It reports that music sales reached a 20-year high in 2024, while video games declined. That does not mean game soundtracks automatically win just because games hardware or software spending softened. But it does suggest something strategically important: if game music is successfully extracted from the game and sold as music, it may be entering a consumer market that is currently in healthier shape than parts of gaming.

That is a useful mindset shift for developers and composers. Instead of asking only, “How does the soundtrack support the game?”, they may need to ask, “How can this music survive and earn outside the game?”

That question opens the door to soundtrack releases, creator-owned publishing, vinyl, live performance, sync, short-form creator content, and catalog thinking.

What this means for creators, publishers, and platforms

For creators, the trend is a reminder that game music should be treated less like disposable production material and more like music IP.

For publishers and studios, it suggests soundtrack strategy should not start after launch. It should be designed earlier: rights structure, metadata, distribution, monetization, and whether the music will have a life outside the game.

The trend of selling or monetizing video game music is really part of a bigger shift: game soundtracks are becoming music assets, not just game assets.

So the real opportunity is not only to write better game music.

It is to treat game music like something worth owning, managing, and monetizing over time.