If you follow the music business closely, Warner Music Group’s fiscal second-quarter 2026 results are worth paying attention to.

Not only because the headline numbers were strong, but because they show something deeper about where value is building in today’s music economy: streaming is still growing, publishing is getting stronger, margins are improving, and catalogs remain important enough for Warner and Bain to deploy serious capital into rights acquisition.

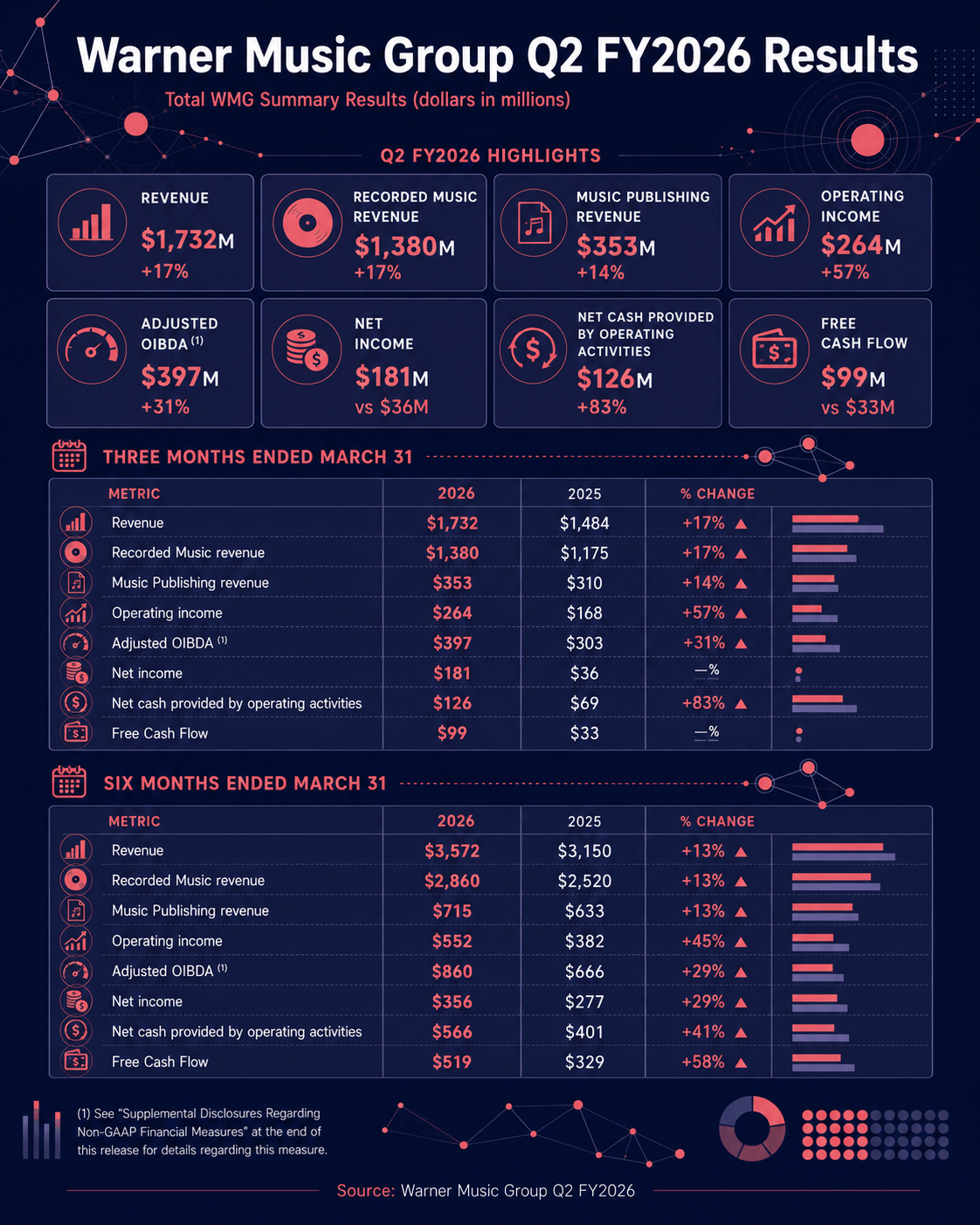

For the quarter ended March 31, 2026, WMG which manage music rights from Bruno Mars, reported $1.732B in total revenue, $181M in net income, $264M in operating income, and $397M in Adjusted OIBDA. Cash provided by operating activities reached $126M, and free cash flow rose to $99M.

The big picture: this was a strong quarter

At the highest level, the quarter was about both growth and efficiency.

Revenue rose 17% year over year, or 12% in constant currency, while operating income rose 57% and Adjusted OIBDA rose 31%. Net income jumped from $36M to $181M. WMG also reported a clear improvement in cash generation, with operating cash flow up 83% and free cash flow up sharply year over year.

This matters because a good music-company quarter is not just about top-line growth. It is also about whether the company is turning revenue into healthier margins and stronger cash flow. In this quarter, Warner did both.

Recorded Music stayed at the center of the story

Recorded Music remains Warner’s largest business by far, and Q2 reinforced that.

The division generated $1.380B in revenue, up 17%, with $975M in digital revenue, $137M in physical, $164M in artist services and expanded-rights, and $104M in licensing.

That mix says a lot. Digital is still doing the heavy lifting, but the business is not purely streaming-only. Physical revenue is still meaningful, artist services remains a growing area, and licensing still contributes even in a quarter where it was slightly lower year over year.

For Tably, this is a useful reminder that modern music monetization is layered. Streaming may dominate, but physical, licensing, and expanded-rights all continue to matter in the wider rights economy.

Streaming growth was strong — and the adjusted story was even stronger

Streaming was one of the most important signals in the quarter.

WMG said total digital revenue rose 16.7%, while total streaming revenue rose 17.1%. In Recorded Music specifically, streaming revenue increased 16.5%. But the more revealing number may be the adjusted one: after excluding the prior-year $11M DSP true-up and settlement payment and the $6M impact of the BMG termination, Recorded Music streaming revenue was up 18.9%, or 14.4% in constant currency.

Warner said that acceleration was driven by per-subscriber minimum increases and continued market share gains. Subscription revenue in Recorded Music, adjusted for those same items, rose 20.9%.

That matters because it suggests the quarter was not just helped by accounting noise or one-offs. The core streaming engine looks stronger than the headline alone might imply.

Music Publishing also had a strong quarter

Music Publishing is smaller than Recorded Music at WMG, but this quarter shows why it remains strategically important.

Publishing revenue rose to $353M, up 14%, while operating income rose to $61M and Adjusted OIBDA to $97M.

The composition of revenue is especially interesting:

- Digital: $224M

- Performance: $58M

- Synchronization: $50M

- Mechanical: $17M

Warner also said Music Publishing streaming revenue increased 20.0%, driven by new deals and renewals plus broader market growth. Performance revenue rose 9.4%, with higher touring and live activity helping the result.

That is important because it shows publishing is not just passively following recorded music. It has its own growth drivers, and they are closely tied to recurring digital usage, live performance, and licensing behavior.

Margins and cash flow improved meaningfully

One of the strongest parts of the quarter was operating leverage.

Adjusted OIBDA margin rose to 22.9% from 20.4%, a 2.5 percentage point improvement. WMG said this was driven by revenue mix and savings from restructuring plans, even after reinvesting part of those savings back into the business.

Cash provided by operating activities rose from $69M to $126M, while free cash flow increased from $33M to $99M. Capital expenditures also declined to $27M from $36M, partly because the prior-year quarter had higher tech investment.

This is one of the most business-relevant signals in the report. Revenue growth is good, but cash-flow improvement tends to make that growth feel more durable. It also gives the company more flexibility for catalog deals, technology investment, and strategic partnerships.

Warner is still betting on catalogs

One of the most interesting lines in the quarter was not about revenue at all. It was about capital allocation.

Warner said its joint venture with Bain acquired $650M in recorded music and music publishing catalogs.

That matters because it reinforces a broader market truth: major music companies are still willing to deploy large amounts of capital into music rights, especially where they see long-term recurring value.

Check our article about artists selling their catalog rights here

What this means for artists, songwriters, and rights holders

For creators and rights holders, Warner’s quarter sends a few clear signals.

First, streaming is still the main growth engine, especially when subscription economics improve and market share expands.

Second, publishing continues to matter a lot, especially where digital, performance, and sync all work together.

Third, catalog ownership still matters, because major companies are continuing to buy rights at scale.

And fourth, efficiency matters. Warner’s quarter was not only about higher revenue. It was about turning that revenue into stronger margins and stronger cash flow.