If you work in music rights, publishing, songwriting or collective management, SGAE’s 2026 budget documents are worth reading closely.

Not because they are easy to read. They are not. But because inside them is a very clear picture of how rights money is expected to move in 2026: where it comes from, which channels now matter most, how much SGAE plans to distribute, and what that says about the current shape of the Spanish music-rights economy.

The big numbers are already telling. SGAE budgets €414.3M in total collection for 2026 and €431.6M in total distribution, while its income statement projects a final budget surplus of €1.39M. The biggest recurrent collection lines are public communication, digital markets, broadcasting and cable, and performing arts and music. On the distribution side, digital markets are the largest category of all.

1. The big picture: SGAE is still a very large rights-distribution machine

The first thing the budget makes clear is scale.

For 2026, SGAE expects €381.5M in recurrent collection, plus €1.97M in administered income, bringing general recurrent collection to €383.5M. Once €30.77M in extraordinary arrears agreements is added, the total collection budget reaches €414.26M. On the other side, the distribution budget reaches €431.64M, made up of €381.07M in recurrent distribution, €37.57M in extraordinary distributions, and €13M in rescues pending documentation.

That gap between collection and distribution is one of the first things readers will notice. The most reasonable reading is that SGAE’s budget is not built as a simple same-year mirror. Distribution includes extraordinary components and documentation rescues that likely reflect prior-period rights flows and settlement timing. That is an inference from the structure of the budgets, rather than something explicitly spelled out in the files.

2. Where the money comes from: the collection mix

The collection budget shows a diversified rights economy, but not a flat one.

The biggest recurrent collection category is public communication (€87.05M). Right behind it are digital markets (€82.77M) and broadcasting and cable (€82.54M). Then comes performing arts and music (€71.61M), followed by private copying (€15.16M) and physical supports (€3.10M).

Inside those large blocks, some lines stand out immediately. In performing arts and music, concerts (€59.22M) make up the overwhelming majority, while dramatic rights sit at €12.38M. In public communication, the largest line is mechanical execution (€60.97M), followed by human execution (€12.38M) and TV receiver devices (€10.26M). In broadcasting and cable, television dominates at €67.94M, far above radio at €14.61M.

3. Digital is no longer secondary

The most important structural point in the collection budget may be digital.

SGAE budgets €82.77M in digital markets for 2026. Within that total, streaming/listens account for €42.53M, audiovisual for €30.66M, and operators of cable, ADSL, mobile TV and similar services for €9.06M. Smaller digital lines include downloads (€142K), mobile melodies (€164K) and webcasting/internet radio (€220K).

That matters because it places digital in the same weight class as broadcast and public communication. It is not a side channel anymore. It is one of the core engines of recurrent rights income.

If you are interested in recurring rights income, try Tably’s Creator Program.

4. Distribution: where SGAE plans to send the money

The distribution budget is where the creator-facing meaning becomes clearer.

The largest recurrent distribution category is digital markets (€90.60M). Then come public communication (€81.92M), broadcasting (€79.19M) and performing arts and music (€73.64M). Private copying is budgeted at €14.17M, physical supports at €2.98M, and international at €38.58M.

.png)

Inside performing arts and music distribution, concerts (€61.19M) dominate. Inside public communication, recorded music (€56.99M) is far larger than live music (€11.85M). In broadcasting, television again leads by a wide margin at €65.16M, compared with €14.03M for radio.

What stands out most is that digital distributes even more than it collects in the recurrent 2026 budget. Collection for digital is €82.77M, while distribution is €90.60M. That does not necessarily mean digital is “overpaying”; more likely it reflects settlement timing and budget treatment. Still, from a creator point of view, the key message is clear: digital is now the largest single distribution category in the SGAE plan.

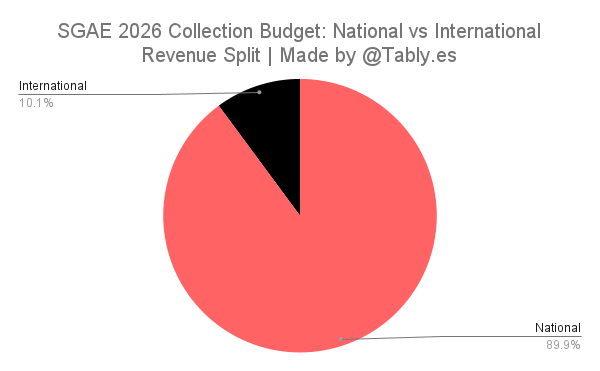

5. National versus international: still mainly Spain

SGAE’s 2026 budget remains heavily national.

Recurrent collection is budgeted at €342.24M national and €39.27M international. Recurrent distribution is budgeted at €342.48M national and €38.58M international.

So while international rights are significant, they are still much smaller than the domestic base. For readers trying to understand creator economics in Spain, that means local licensing structures remain central to the system.

6. The income statement: stable, but not oversized

The SGAE's P&L adds another useful layer. It shows that SGAE’s internal operating margin is not huge, even though the society handles very large distribution volumes.

For 2026, SGAE budgets €63.97M in operating income and €61.45M in operating expenses. Staff costs account for €31.79M, while other operating expenses account for €27.39M, and governance/aid expenses for €2.27M. That leaves €2.53M before amortization. After €2.80M in amortization, the activity result becomes -€275K. Financial income, financial expenses and other results then bring recurrent surplus back to €489K. With extraordinary income and extraordinary costs included, the final expected budget surplus is €1.39M.

One especially important legal-budget note is that €15.4M in prescription is expected in 2026, but the document says it is not counted in the total budget surplus because it must first be used to offset negative surpluses under the applicable legal article.

7. What this means for songwriters, composers, publishers and rights holders

For creators, the report says three things.

First, SGAE’s economic model is still broad-based. It is not dependent on one channel alone. Live, public communication, TV, radio, digital and private copying all still matter.

Second, digital is now central. It is one of the biggest collection sources and the biggest distribution category. That makes digital rights visibility, metadata quality and exploitation strategy more important than ever.

Third, distribution still depends on administrative and legal structure. The gap between collection and distribution categories reminds us that rights money does not move in a perfectly linear way. Timing, documentation, extraordinary agreements and prior-period settlements all shape what creators ultimately receive.

For Tably readers, this supports a wider idea that already appears across your own site: music rights work best when creators have more transparency into how value is generated, distributed and retained. That is why linking this article to your FAQs and your recent article on music rights and buyout contracts in Europe would be useful both for readers and for internal topical authority. Tably’s FAQ explains your royalties-based model in plain language, while the buyout article expands the conversation toward long-term creator rights and recurring income.

Sources:

- Presupuesto SGAE 2026 - Cuenta de resultados

- Presupuesto SGAE 2026 – Ingresos sociales

- Presupuesto SGAE 2026 – Derechos repartidos